In this episode of World Economics we discuss the concept of helicopter money, the mistake of using the Hong Kong example and why it is likely to be implemented… and fail.

In this episode of World Economics we discuss the concept of helicopter money, the mistake of using the Hong Kong example and why it is likely to be implemented… and fail.

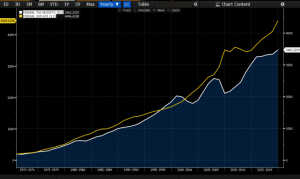

Every time there is a budget debate, politicians from both parties will discuss the deficit and spending as if the first one did not matter and the latter could only increase. However, the main problem of the US budget in the past four decades is that total outlays rise significantly faster than receipts no matter what the economic growth or revenue stream does. For example, in the fiscal years 2018 and 2019 total outlays rose mostly due to mandatory expenses in Social Security, Medicare, and Medicaid. No tax revenue measure would have covered that amount.

Total outlays were $4,447 billion in 2019, $339 billion above those in FY 2018, an 8.2 percent increase. No serious economist can believe that any tax increase would have generated more than $300 billion of new and additional revenues every year.

The idea that eliminating the tax cuts would have solved the deficit is clearly debunked by history and mathematics. There is no way in which any form of revenue measure would have covered a $339 billion spending increase.

No serious economist can believe that keeping uncompetitive tax rates well above the average of the OECD would have generated more revenues in a global slowdown. If anything, a combination of higher taxes and weaker growth would have made the deficit even worse. Why do we know that? Because it is exactly what has happened in the Eurozone countries that decided to raise taxes in a slowdown and it is also what all of us witnessed in the United States when revenue measures were implemented.

The US was maintaining a completely uncompetitive and disproportionately high corporate income tax (one of the highest in the world) and all it did was to make it similar to other countries (the Nordic countries have corporate income tax rates of 21.4% Sweden and 22% Denmark, for example).

What happened to corporate tax receipts before the tax cut? The evidence of a weakening operating profit environment: Corporate tax receipts fell 1% in 2017 and 13% in 2016. The manufacturing and operating profit recessions were already evident before the tax cuts. If anything, reducing the corporate rate helped companies hire more and recover, which in turn made total fiscal revenues rise by $13 billion to $3,328 billion in the fiscal year 2018, and rise by $133 billion in 2019, to $ 3,462 billion, both above budget, according to the CBO. Remember also that critics of the tax cuts expected total receipts to fall, not increase.

Mandatory spending is now at $2 trillion of a total of $4.45 trillion outlays for the fiscal year 2019. This figure is projected to increase to $3.3 trillion by 2023. Even if discretionary spending stays flat, total outlays are estimated to increase by more than $1 trillion, significantly above any measure of tax revenues, and that is without considering a possible recession.

Any politician should understand that it is simply impossible to collect an additional $1 trillion per year over and above what are already record-high receipts.

For 2020, tax receipts are estimated at $3,472 billion compared to $4,473 billion in outlays, which means a $1,001 billion deficit. With outlays consistently above 20% of GDP and receipts at 16.5% average, anyone can understand that any recession will bring the gap wider and deficits even higher.

Deficits mean more taxes or more inflation in the future. Both hurt the middle class the most. More government spending means more deficit, more debt, and less growth.

When candidates promise more “real money” for higher spending they are not talking of real money. They talk of real debt, which means less real money into future schools, future housing, and future healthcare at the expense of our grandchildren’s salaries and wealth. More government and more debt is less prosperity.

Anyone who thinks that this gap can be reduced by massively hiking taxes is not understanding the US economy and the global situation. It would lead to job destruction, corporate relocation to other countries and lower investment. However, even in the most optimistic estimates of tax revenues coming from some politicians, the revenue-spending gap is not even closed, let alone a net reduction in debt. The proof that the US problem is a spending issue is that even those who propose massive tax hikes are not expecting to eliminate the deficit, let alone reduce debt, that is why they add massive money printing to their magic solutions.

Now, let us ask ourselves one question: If the solution to the US debt and deficit is to print masses of money, why do they propose to increase taxes? If printing money was the solution, the Democrats should have massive tax cuts in their program. The reality is that neither tax hikes nor monetary insanity will curb the deficit trend.

No tax hike will solve the deficit problem. Even less when those tax hikes are supposed to finance even more expenses. No amount of money printing will solve the financial imbalances of the US, it only increases the problem. If money printing was the solution, Argentina would be the highest growing economy in the world.

If the US wants to curb its debt before it generates a Eurozone-type crisis that leads to stagnation and high unemployment, the government needs to really cut spending, because deficits are soaring due to ballooning mandatory outlays, not due to tax cuts.

Market participants’ excess of optimism with the trade agreement between the United States and China is clearly exaggerated, once we have the details. Read More

In this interview, we discuss the economic developments of 2019 and the outlook for 2020.

Watch the interview with Victoria Scholar at IG TV.

My book “Escape from the Central Bank Trap” is available now on my Amazon Page.

Article published at the World Economic Forum. Read More

Watch the entire interview here talking about the Rising Challenges of the European Union

This is a video excerpt from my keynote speech at the Bloomberg annual conference “The Next Big Thing”.

This is an exclusive “Hedgeye Investing Summit” interview between Daniel Lacalle, chief economist and investment officer at Tressis Gestion and Hedgeye CEO Keith McCullough. Read More

The Federal Reserve has injected $278 billion into the securities repurchase market for the first time. Numerous justifications have been provided to explain why this has happened and, more importantly, why it lasted for various days. The first explanation was quite simplistic: an unexpected tax payment. This made no sense. If there is ample liquidity and investors are happy to take financing positions at negative rates all over the world, the abrupt rise in repo rates would simply vanish in a few hours. Read More

Negative rates are likely one of the reasons behind the lacklustre European growth. Negative rates have worked as a tool to transfer wealth from savers to the indebted governments that have abandoned all structural reforms, while these extremely low rates have also perpetuated overcapacity, incentivised the refinancing of zombie companies and effectively worked as a disguised subsidy on low productivity. Not only those measures have damaged banks, but they have also created very dangerous collateral impacts (read “Negative Rates Have Damaged Banks But This Is Not The Worst Effect”).

In recent weeks we have heard of a likely new stimulus plan that would include a new repurchase program and further rate cuts. A new asset purchase program is completely unnecessary and unlikely to spur growth when all Eurozone countries already have sovereign debt with negative yields in 2-year maturities and the vast majority have negative real or nominal yields in the 10-year bonds. Why would the ECB repurchase corporate and sovereign bonds when the issuers are already financing themselves at the lowest rates in history? Furthermore, by reading some statements one would believe that the ECB has stopped supporting the economy. Far from it, when it repurchases all debt maturities in its balance sheet and has implemented another liquidity injection TLTRO in March 2019.

The main problem of those who defend further purchases and more negative rates is one of diagnosis. The central planners believe the Eurozone problems come from lack of demand, and that investment and credit growth are not what they would want them to be only because investors and corporates believe that rates will ultimately rise, leading to defensive positioning.

The eurozone has seen nothing but demand-side stimuli, and after trillions of euros the economy is weakening because of them, not despite them. Because the problem is a supply-side problem that the ECB cannot solve. Rising interventionism and tax wedge that choke the private initiative despite alleged attractive conditions.

The other problem of diagnosis is to believe that credit growth and investment today are insufficient. There is no evidence that companies are investing less than what they need or that citizens are not taking the credit they desire and are able to repay, rather the opposite. In fact, the rise of zombie companies that the BIS mentions in various papers is precisely a sign of malinvestment and excess capacity. Ultimately, the central planners who believe that credit and investment growth are insufficient think so because they ignore technology and aging of the population. When governments and central banks ignore the diminishing requirement of capital investment that technology creates and the changes in consumption and investment patterns from demographics, their diagnosis of what is adequate investment and consumption is simply wrong. Even worse, when the rationale to support the idea of “lack of investment” and therefore a need for lower rates is based on looking at 2001-2007 as “normal” years, they are always going to make a mistake. Those were years that no one should consider as average, but years of a bubble that burst badly.

A recent analysis made by Scope Ratings showed that “a tiered system of remunerating reserves to mitigate the impact of lower rates on bank profits will have a limited effect. Euro Area banks have already incurred EUR 23.2bn in charges since the negative-rate began policy in 2014, EUR 7.5bn in 2018 alone”. Scope calculates the annualized current running cost of excess liquidity is EUR 6.8bn. Any further cut to the deposit rate would cost EA banks EUR 1.7bn. “In other words, EA bank ROE is c.40bp lower than it would be in the absence of negative rates.

Why should the ECB raise rates by a small 25bps then?

The evidence of the last years shows that the eurozone is slowing down in the middle of an unprecedented chain of fiscal and monetary stimuli. The failure to improve growth cannot be detached from the persistence on repeating failed measures. Implementing a larger quantitative easing and deeper rate cut program will not solve it, because the diagnosis is incorrect.

A small rate hike added to support to those governments that implement structural reforms may help the eurozone. Monetary policy now is dangerously whitewashing populists who feel they can increase imbalances and put further fiscal strains on their countries’ budgets with no real risk, as yields continue to fall, albeit artificially.

A small rate hike would be a healthy signal that may help the ECB understand the real secondary demand for sovereigns, stop the zombification of the economy and improve liquidity transmissions to the real economy. Instead of being an incentive for reckless behavior from deficit-spending governments, it can be the beginning of an incentive to strengthen the private sector and the real economy.

![]()

© 2026 Alpha Strategy Consulting. Privacy Statement