While markets become increasingly bullish, oil prices are close to a “warning zone” where the barrel could be one -if not the only- catalyst of a major slowdown.

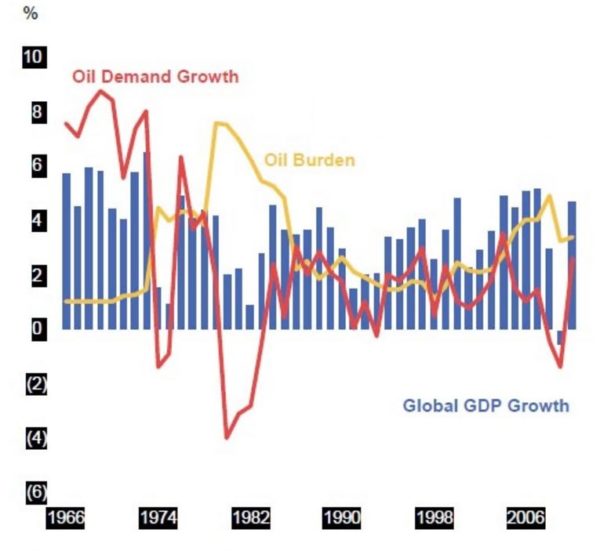

In my book “Escape from the Central Bank Trap”, I explain the concept of the “Oil Burden”. It is the percentage of global GDP spent on buying oil. It is often said that when the oil burden reaches 5-6% of GDP it can be a cause of a global slowdown.

The mistake that many make is to think that the oil burden is a cause and not a symptom.

In the past, we have seen that a period of abrupt increases in oil prices was followed by a recession or a crisis. However, not because oil prices rose rapidly, but because the dramatic increase in commodities’ prices was caused by a bubble of credit and excess monetary stimuli.

In reality, the oil burden is perfectly manageable at 5% of GDP because the energy intensity of GDP growth is diminishing. We are less dependent on energy to create growth in the economy.

Global energy intensity (total energy consumption per unit of GDP) declined by 1.2% in 2017, slightly below its historical yet unstoppable trend (-1.5%/year on average between 2000 and 2017 and -1.8% in 2016). In fact, global energy intensity is down 54% since 1990.

So the problem is not the oil burden by itself but the cause of the price spike.

When oil prices rise abruptly we should be concerned, because they can cause a domino effect on the real economy. When the reason for the price increase is not fundamental, we have a major problem.

Why are oil prices rising abnormally in recent months?

. Supply manipulation. Despite inventories falling, OPEC has maintained a tight grip on supply, unjustified from the premise of an oil glut that is inexistent or from the premise of “low” prices, which are comfortably above $70 a barrel. By being greedy and keeping supply tight, OPEC is hurting its customers -mainly Europe- and creating the foundations of a forthcoming bust cycle.

. Iran sanctions. The reality is that Iran sanctions have a very small impact on the supply market, 600,000 barrels a day reduction in exports. These could be easily offset by higher OPEC and non-OPEC output, but if supply limits remain, the impact on marginal prices is exaggerated. OPEC produced 32.79 million barrels per day in August, up 220,000 bpd (barrels per day)from July’s revised level and the highest this year. However, the lid remains on the maximum output despite Libya coming back to normalized levels.

. Venezuela production collapse. The Maduro regime’s disastrous management of the state-owned PdVSA has led the country to cut production to 1.4 mbpd (million barrels per day) and likely end 2018 at 1mbpd. The combined impact of Venezuela and Iran could have easily been offset by higher Saudi and OPEC production, helped by higher non-OPEC output.

. Inventories continue to fall. Crude inventories fell for the fifth consecutive week. Stocks are at 394.1 million barrels at the end of the week (22nd Sept 2018) in the US, the lowest level since early 2015. OPEC cannot hang on to the message of an oil glut. It is not evident anywhere anymore.

. US oil production continues to rise and provide positive surprises. U.S. crude oil production is expected to rise 1.31 mbpd to 10.68 mbpd in 2018, according to the U.S. Energy Information Administration. Production will average 11.7 mbpd in 2019.

. What about demand? High prices are already affecting oil demand in India and Europe. India total demand fell month-on-month in July. Demand was 358 kb/d lower, and demand growth has stalled. In Europe, a slowdown in industrial production and consumer spending is evident, while the emerging market crisis and China slowdown are also clear risks to the optimistic expectations of demand growth posted by OPEC and the EIA.

The risk, therefore, is that too much greed may break the camel’s neck. Imposing artificially higher prices on the world through supply management always backfires. Many oil analysts wonder why oil is not at $100 a barrel with all the above-mentioned issues.

The supply management’s desired “boom” is smaller than expected due to lower energy intensity and high global debt, and the risk of an abrupt bust is exacerbated because price increases are not based on fundamentals.

The global oil burden will rise to 3.1% of global GDP in 2018 from 2.4% in 2017 and -if Brent goes to $80 for an entire year- could soar to 4% of global GDP. This is deemed as manageable by most analysts. However, “manageable” is a scary concept that was used numerous times in the past before a bust.

The risk for the economy may not be the oil burden in itself, but a rising oil burden that is entirely driven by supply manipulation, disconnected from supply and demand reality and affordability.

If you believe rising oil prices prove the success of OPEC’s boom cycle creation, be careful about the bust. It will be self-inflicted.